History of the CFTC and COT Report

Feb 17, 2026

The Commitment of Traders report is one of the longest-running public datasets in financial markets. The CFTC has been publishing some form of trader positioning data since 1962. Understanding where it came from clarifies what it was designed to do — and what it was not.

The Origins: Grain Market Oversight

The regulatory roots of the COT report go back to the early 20th century, when grain markets were a focal point of US economic policy.

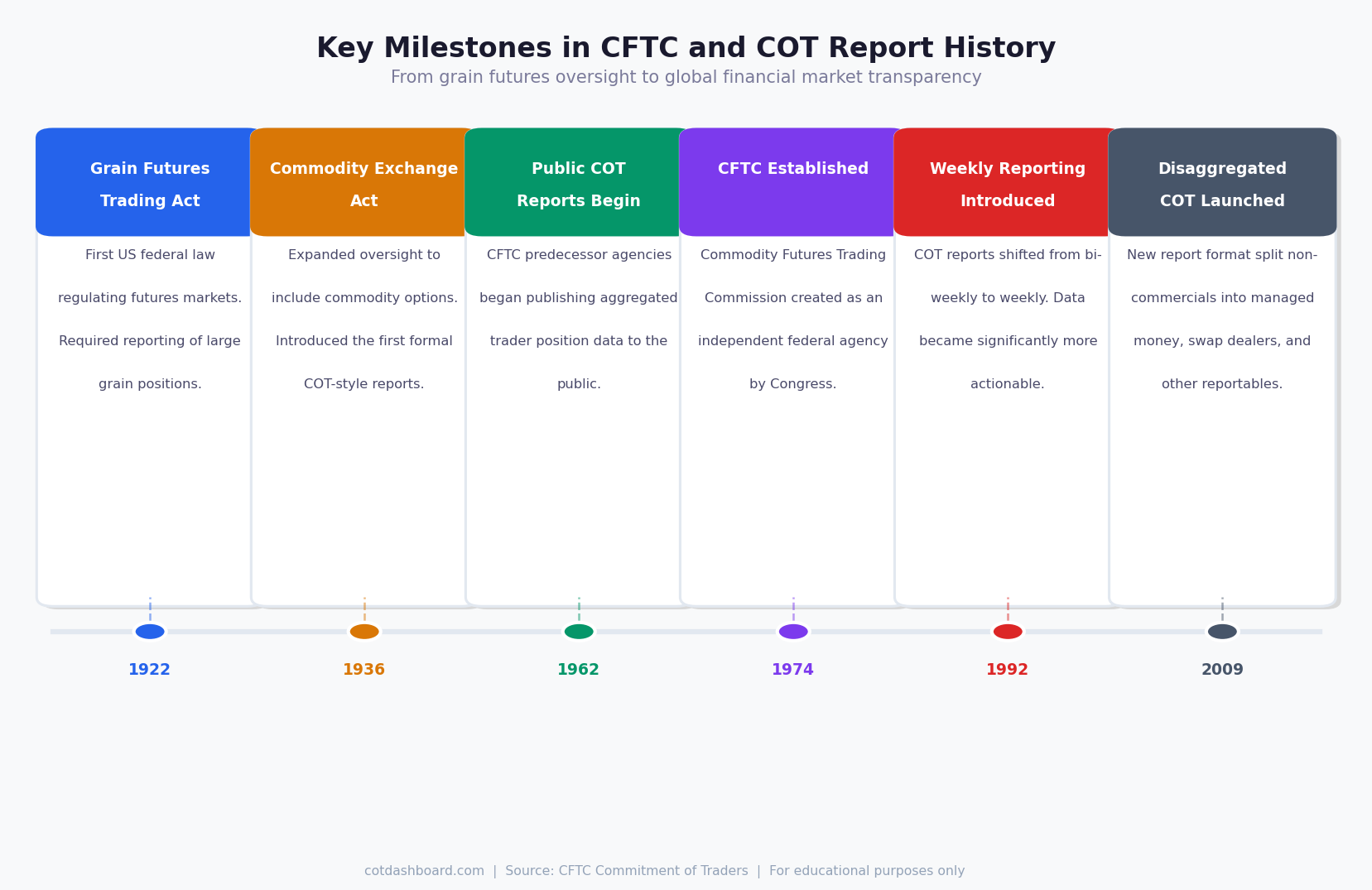

The Grain Futures Trading Act of 1922 was the first significant federal law governing futures markets. It required large grain traders to report their positions to regulators. The stated purpose was to detect and deter market manipulation — not to provide a public sentiment indicator.

The Commodity Exchange Act of 1936 expanded this framework to cover additional commodities and introduced restrictions on certain speculative activities. Position reporting continued under these rules, though the data was primarily used internally by regulators.

The CFTC Is Established: 1974

The modern era of futures regulation began with the Commodity Futures Trading Commission Act of 1974, which created the CFTC as an independent federal agency.

Before 1974, futures oversight was split between the Department of Agriculture (for agricultural commodities) and the Securities and Exchange Commission (for financial instruments). The creation of the CFTC consolidated oversight under one agency and extended it to cover the growing number of financial futures products.

The CFTC formally took over COT reporting from its predecessor agencies and continued the practice of publishing aggregated trader position data.

COT Goes Weekly: 1992

The frequency and format of COT reports changed significantly over the decades.

Early reports were published monthly, then bi-weekly. In 1992, the CFTC shifted to weekly publication — positions as of Tuesday, published the following Friday. This 3-day lag has remained the standard ever since.

The weekly cadence made the data substantially more useful to analysts tracking how positioning was changing in response to market events. A monthly snapshot captures almost nothing about intra-month shifts in sentiment.

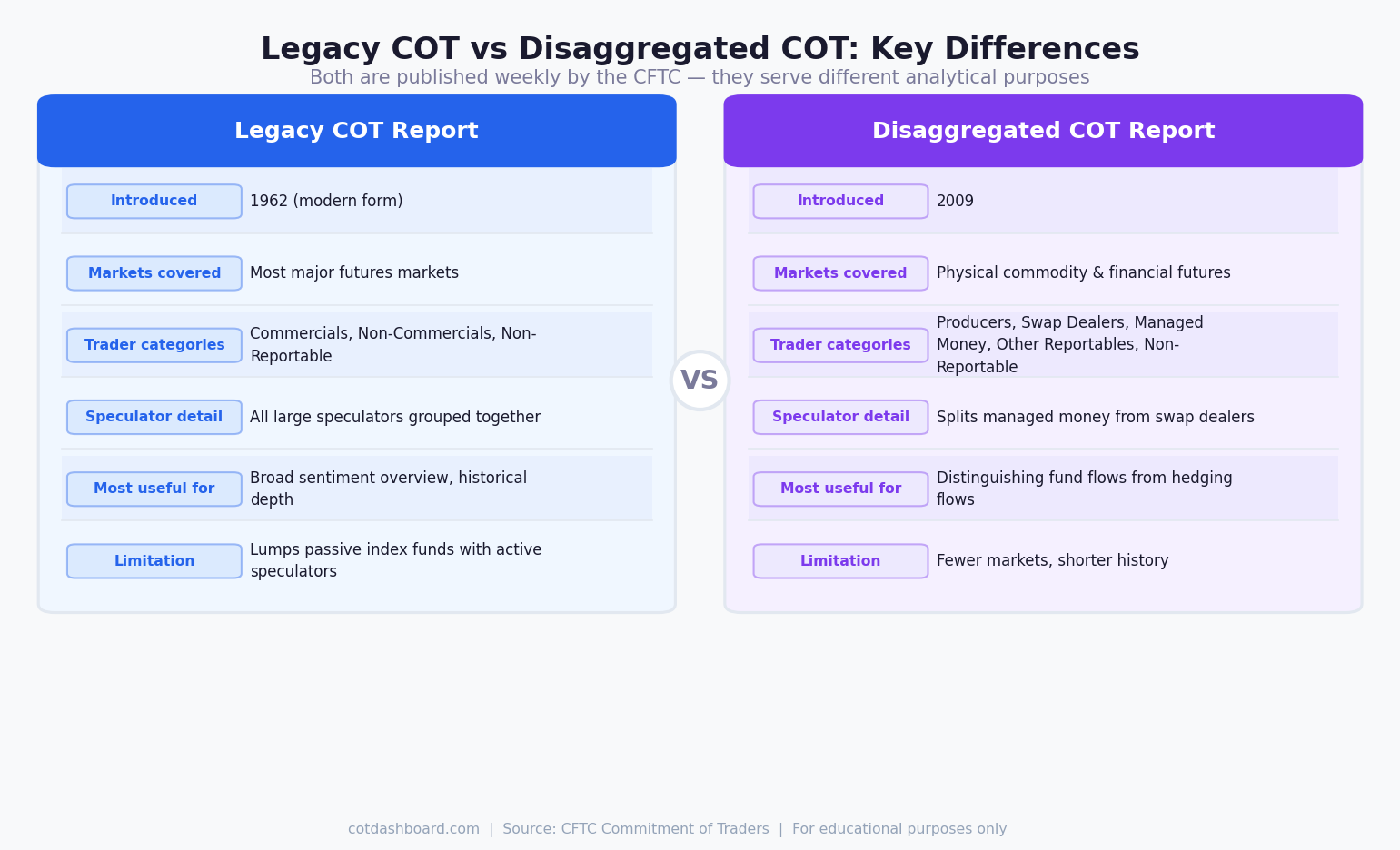

The Legacy COT Format

The "legacy" COT report — still published today — divides market participants into three categories:

- Commercials — entities with a demonstrated hedging purpose

- Non-Commercials — large speculators with no hedging purpose

- Non-Reportable — everyone below the reporting threshold

This format remained largely unchanged from the 1960s through the 2000s. It works well for identifying broad speculative sentiment but has a structural problem: it lumps very different types of non-commercial participants together.

A passive commodity index fund that simply buys and rolls futures is classified identically to an active macro hedge fund taking a strong directional view. Their implications for market sentiment are very different.

The Disaggregated Report: 2009

In 2009, the CFTC introduced the Disaggregated COT report to address this limitation.

The new format split the old non-commercial category into four groups:

- Producer/Merchant/Processor/User — physical market participants (equivalent to commercials)

- Swap Dealers — financial intermediaries, often running commodity index exposure

- Managed Money — hedge funds and CTAs with active directional strategies

- Other Reportables — large traders that don't fit the other categories

This separation allowed analysts to distinguish between passive index-driven flows (swap dealers) and active speculative positioning (managed money) — a distinction invisible in the legacy report.

The disaggregated format covers physical commodity and selected financial futures markets. It does not cover all markets in the legacy report, and its history only extends back to 2006.

Which Format Is Used Most

For most practical COT analysis, the legacy report remains the standard.

Reasons include:

- Longer historical record (usable data back to the early 1990s for most markets)

- Broader market coverage, including FX, equity indices, and Treasuries

- Simpler structure — easier to compare percentile ranks across markets consistently

The disaggregated report is more useful when you specifically want to separate managed money from passive index flows — relevant in agricultural and energy commodities where commodity index exposure is large.

The cotdashboard.com platform uses the legacy COT format with a 104-week rolling percentile window. This gives consistent, comparable readings across all markets in the dataset.

CFTC Data Today

The CFTC now publishes COT data every Friday at 3:30 PM Eastern Time, covering positions as of the previous Tuesday. The data is freely available at cftc.gov in CSV and legacy text formats.

The agency also publishes:

- Traders in Financial Futures (TFF) — similar to the disaggregated report but focused on financial futures

- Cotton On-Call — specific to cotton markets

- Index Investment Data — tracks commodity index fund exposure quarterly

For the vast majority of COT analysis, the standard Legacy or Disaggregated weekly reports are what analysts use.

For related reading, see What Is the COT Report? and Commercial vs Non-Commercial Traders: What's the Difference?